Originally Posted on CUInsight

Is the Community Charter Truly Dead?

I am going to tell you a secret I recently discovered about credit union chartering that (almost) no one else knows. Federal SEG based credit unions can serve larger communities than practically any other charter, including virtually any state charter. The largest credit unions could serve multiple entire states under a federal multiple common bond or SEG based charter.

To explain this secret, the secret of underserved rural districts, requires me to go into an overview of a lot of credit union chartering jargon, the United States’ demographics, and summarization of what happens when you apply math and computing power to the federal charter field of membership rules. It is a long read, but I believe you will find it worthwhile.

Chartering & Field of Membership

Credit unions benefit from a dual chartering system, because the NCUA and state regulators compete for credit unions to operate under their respective charters. Each regulator periodically modernizes its charter to make it more attractive. Federal credit unions may have a slight edge as they benefit from a broader tax exemption and federal pre-emption, which generally means they pay lower taxes, aren’t subject to some state regulations that conflict with federal regulations, have an easier time engaging in multistate branching and FOMs, and only answer to one regulator. However, historically, the perception has been that state charters have benefited from having more liberal field of membership rules. However, that is about to change.

The Key: Underserved Areas (Rural Districts)

My favorite characteristic about this strategy is it rewards credit unions that serve the communities most in need of additional access to financial services – underserved areas and underserved rural districts in particular. However, this strategy is only available to credit unions with a multiple common bond charter and likely most valuable to federal multiple common bond-chartered credit unions. While a Community Charter serves a single community that meets one of the above definitions of a community, a Federal Multiple Common Bond Charter can serve an infinite number of underserved communities as long as they have the ability and intent to serve them.

Each community that a multiple common bond credit union adds to its field of membership must meet the NCUA’s definition of a community as well as an underserved area. You can read a lot more about each of those definitions by following their respective links, but generally speaking that means that the area must meet the following criteria:

Be “economically distressed,” meaning:

- The unemployment rate is at least 1.5 times the national average; or

- At least 20 percent (20%) of the population lives in poverty; or

- The Median Family Income (MFI) is at or below 80% of

- For units within a statistical area: either the MFI of the corresponding Metropolitan Statistical Area or of the national MFI for Metro Areas, whichever is greater; or

- For units outside of any statistical area: either the corresponding state’s Non-Metro MFI or the national MFI for Non-Metro Areas, whichever is greater;

Be “underserved by depository institutions,” meaning:

- The concentration of depository institution facilities among the population of the proposed area’s “non-distressed’’ tracts— which sets a benchmark level of adequate service—is greater than the concentration of facilities among the population of all of the proposed area’s census tracts combined.

- If all of its units are within counties designated as “underserved” by the CFPB.

AND either qualify as well-defined local community or a rural district:

- Local Well-Defined Community

- Single Political Jurisdiction

OR - Statistical Area, or a portion thereof, with a population of 2.5 million or less people.

- Rural District

- The total population of the proposed district does not exceed 1,000,000.

AND - Either more than 50% of the proposed district’s population resides in census blocks or other geographic units that are designated as rural by either the Consumer Financial Protection Bureau or the United States Census Bureau,

OR - The district has a population density of 100 persons or fewer per square mile.

Identifying qualifying areas is very complicated so, up until now, underserved areas that credit unions have identified and added to their field of membership generally represent a portion of a community that a credit union could add as a community charter. Take Augusta, Georgia for example:

That all changed when we started using computers to draw the maps for us.

The Strategy, Math, and Computers

We discovered the secret value of underserved areas, and underserved rural districts in particular, when we were working on a proposal for a prospective credit union. We had a prospective client that wanted to expand. However, they already served an entire CBSA and many of its immediately adjacent counties and had been told by multiple experts that they already had the largest possible community under a federal charter. Their market crossed two states, so going state-chartered wasn’t an option. Also, their board, understandably, did not want to give up the majority of their existing community simply to be given the flexibility to go into a new market, where they would also only be able to serve a single small, underserved portion of the new market. Our goal was to give the credit union the flexibility a multiple common bond charter provides, without losing the credit union any part of their existing community. This is how we figured out that they could keep their entire existing market and have the freedom to expand further as a federal multiple common bond.

After looking at a map of the target market for a while, we realized how it could be done. We could use multiple underserved rural districts, which collectively would cover the entire market and more. This strategy would allow the credit union not only to expand into surrounding areas but also the freedom to enter entirely new markets, merge with credit unions outside of their existing market, and even potentially buy banks.

Under this strategy, the number of branches, or service facilities, your credit union has, and their location down to the census block group has a significant impact on your potential field of membership. For each service facility a credit union has, it can have a separate underserved area. The more branches a credit union has, the more variations and unique areas can be used to obtain the entirety of a target market.

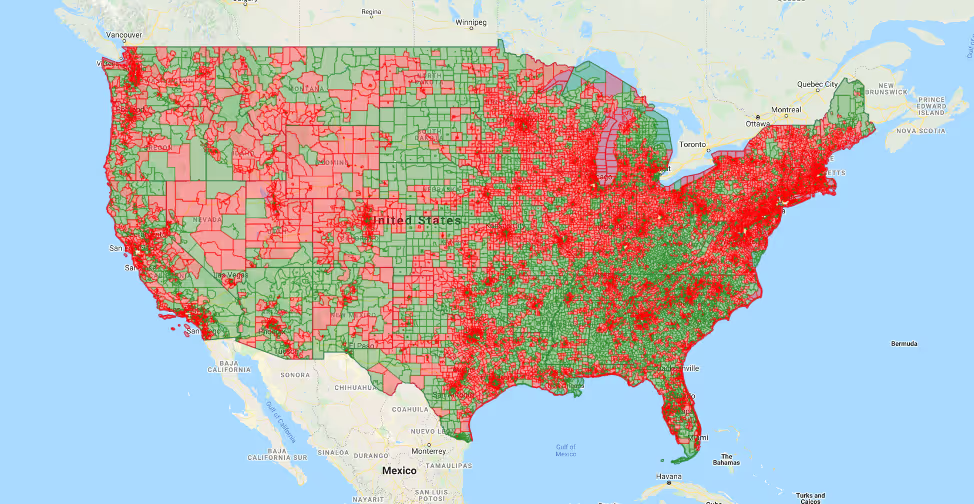

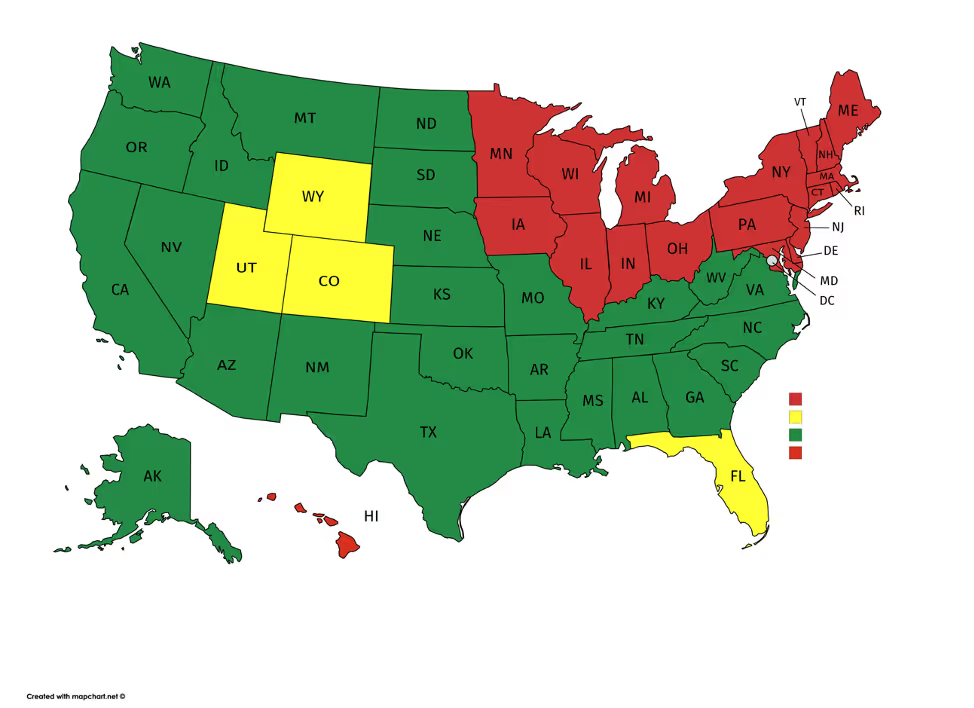

If you look at the map of the United States below, this strategy will work for almost the entire country except for New England and the Midwest, which present possibly insurmountable demographic hurdles (depending on what area you are trying to prioritize).

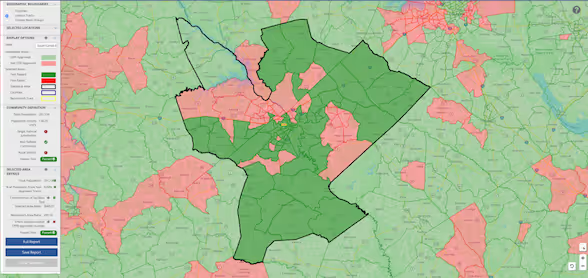

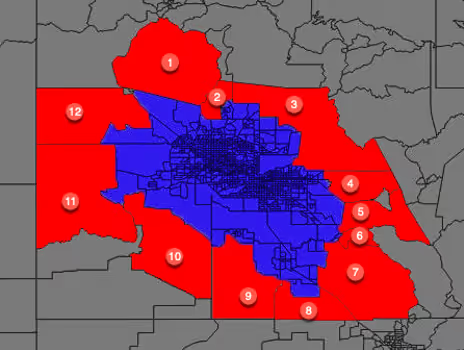

Another problem we faced implementing this strategy we call the “outer ring” problem. This problem arises when an outer ring of units (census tracts or more likely now census block groups) present a bottleneck that prevents the use of enough underserved rural districts from being used to obtain a desired community. Take Phoenix, Arizona, for example.

Inside the highlighted ring of census tracts, there are 2,456,176 residents who live in non-distressed areas. You would need 17 separate underserved rural districts to cover the entire market. However, you can see that there are only 12 different census tracts that make up the “outer ring” so there aren’t enough paths to leverage qualifying underserved rural districts from the surrounding areas to pick up the residents in the “non distressed” units in the community.

There are two things you can do to solve this problem. First, define the area by the smallest possible permissible units: census block groups, which opens up a few more paths into the market. Second, use local well-defined underserved areas to reduce the number of residents that need to be picked up by surrounding underserved rural districts. This way, the 12 different entry points to the market ends up being enough to get the entire CBSA and ultimately allows a credit union to get the whole state of Arizona under a federal charter.

Here is a map that provides a quick cheat sheet to the value that this strategy offers to credit unions in each state: Green- CUs can serve the whole state, Yellow- CUs can possibly serve the whole state, Red-CUs cannot serve the whole state.

While not as groundbreaking, the federal multiple common bond charter and underserved areas still provide a lot of value and growth opportunities to credit unions in New England or the Midwest and should not be discounted.

Conclusion

Thank you for reading this much. It was a long read. I hope you found this interesting. Discovering this secret was a labor of love for me. I hope you find it valuable to your credit union or at least that it makes you reexamine things that you have been told are impossible, because when it comes to field of membership anything is possible as long as you have the ability and intent to do it (unless you are in New England or certain states in the Midwest – Sorry!). Also, please remember that while this strategy unlocks dramatically larger communities under a federal multiple common bond charter, your credit union would still need to have the ability and intent to serve the areas you apply to serve. So don’t waste your time or the NCUA’s Office of Credit Union Resources and Expansion applying for a larger area than you actually plan or have the ability to serve.