Learn about underserved areas and the field of membership opportunities they could offer your credit union.

What is an Underserved Area?

Only Multiple Common Bond Charters have the option of adding “underserved areas” to their field of membership (FOM). As provided in the Federal Credit Union Act, an underserved area is:

(1) a “local community, neighborhood, or rural district” that (2) meets the definition of an “investment area” under section 103(16) of the Community Development Banking and Financial Institutions Act of 1994 (“CDFI”), 12 U.S.C. 4702(16), and (3) is “underserved by other depository institutions” based on data of the NCUA Board and the federal banking agencies.

In simpler terms, as the National Credit Union Administration (NCUA) lays out in its provided guidance on expanding service to underserved areas, the area must:

–Be a local community;

–Meet the standards of economic distress to qualify as an investment area;

–Have significant unmet needs, and

–Be underserved by other depository institutions.

Underserved areas can be added irrespective of location, with one limitation: an underserved area based on a rural district must be located within either the credit union’s headquarters’ state or adjoining states.

How Does Adding an Underserved Area Affect a Credit Union’s Charter?

Adding an underserved area to an FOM will not change the charter type of a multiple common bond credit union. Further, more than one such institution may serve the same underserved area. The addition likewise does not alter the credit union’s eligibility for the benefits associated with a Low-income Designation (LID).

How Does an Area Qualify as a Local Community?

A credit union must prove through its application to the NCUA that an underserved area meets the threshold of a well-defined local community, neighborhood or rural district. To do so, it must first define the area as either a “presumed community” or “non-presumed community.”

A presumed community is one that meets any of the following standards by being:

–A single political jurisdiction or portion thereof;

–A combined statistical area or core-based statistical area or a portion thereof with a population at or below 2.5 million people;

–A rural district with a population of 1 million or less; or

–An area the NCUA previously determined is a local community (area must still re-qualify based on economic distress standards).

For a non-presumed community, it falls upon the credit union to demonstrate that there exists sufficient “common interests or interaction” within the area in order for it to qualify. To do so, it must submit a narrative application to the NCUA, which provides “compelling evidence that supports how the area’s residents interact or share common interests.”

In addition, it must outline precise geographic boundaries for the area as well as provide Census Bureau data to determine its total population.

What Qualifies as an Investment Area?

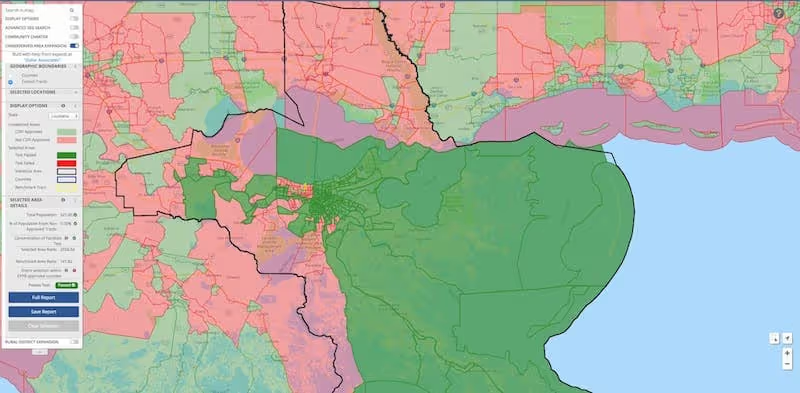

A credit union must likewise demonstrate an underserved area qualifies as an “investment area” according to the definition established in the Community Development Banking and Financial Institutions (CDFI) Act. This is typically done by identifying a contiguous group of Census tracts in which 85% of the population can be shown to live in tracts specifically designated as “economically distressed” based on criteria developed by the Treasury Department’s CDFI Fund related to U.S. Census Bureau data.

To attain the designation, an area must meet at least one of the CDFI’s markers of economic distress:

–Encompassed or located in an empowerment zone or enterprise community designated under section 1391 of the Internal Revenue Code of 1996 (26 U.S.C. 1391);

–Percentage of population living in poverty is at least 20 percent;

–Within a metropolitan area where the median family income is at or below 80 percent of the metropolitan area median family income or the national metropolitan area median family income (whichever is greater);

–Located outside of a metropolitan area where the median family income is at or below 80 percent of the statewide non-metropolitan area median family income or the national non-metropolitan area median family income (whichever is greater);

–Unemployment rate is at least 1.5 times the national average;

–Located outside of a metropolitan area with a county population loss between the most recent decennial census and the previous decennial census of at least 10 percent; or

–If located in a county outside of a metropolitan area, the county net migration loss during the five-year period preceding the most recent decennial census is at least five percent.

Census data must once again be provided to show which qualification(s) is met as well as further prove 85% of the proposed area’s residents indeed reside within one of these distressed tracts.

Significant Unmet Needs

To fully meet the investment area criteria, the community must also display “significant unmet needs for loans or one or more of the financial services credit unions are authorized to offer.” To prove this, an institution must provide evidence of “the credit or depository need with objective reasons and supporting documentation derived from an identified, authoritative source of the federal credit union’s choice.”

Further, in the application process, a credit union is required to directly address how it will fill this precise need within the area.

How Do You Prove an Area is Underserved by Other Depository Institutions?

A proposed service area must also be “underserved by other depository institutions,” thus evidencing the need of the credit union’s services. This is ultimately determined by the area’s “concentration of facilities ratio,” a calculation arrived at by comparing the concentration of depository institution facilities among the population of the area’s non-distressed census tracts against the area’s total tracts combined.

The “underserved” threshold is met simply when the ratio for the non-distressed tracts—considered as a benchmark of adequate service—is greater than that of the proposed community as a whole. If an area does not contain any non-distressed tracts, a neighboring non-distressed tract may be used instead to establish the benchmark ratio.

In lieu of this metric, a credit union may also submit data of its own choosing, provided it is obtained from either the NCUA or other Federal banking agencies, to prove the area is indeed underserved.

Lastly, an area already designated as an “underserved county” by the NCUA based on data from by the Consumer Financial Protection Bureau will also qualify.

Service Facility Requirement

When a credit union adds an underserved area to its FOM, it must, within two years of being approved to do so, establish and maintain an accessible service facility within the community. This could take the form of a branch or mobile branch, a regularly operated office, or an electronic facility such as a video teller machine or kiosk.

In order to qualify as such, a location must accept deposits, take loan applications, and disburse loan proceeds. A credit union need not maintain an ownership stake in the facility, however it must at least participate—for example in a shared branch location—to be considered valid.

The Application Process

Adding underserved areas can be an arduous and complicated process, however it can also provide an enormous advantage in terms of membership growth by combining both common bond groups and communities under one charter. It is a process best confronted with the assistance of an experienced party as understanding the best strategy for your credit union can be both difficult and time-consuming.

At CUCollaborate, we provide a tailored approach to growth based on data-driven insights and specialized software to help credit unions reach the largest target market possible.

Contact us today to learn about our Field of Membership Consulting Services or click below to meet directly with a member of our team for an Opportunity Assessment for your credit union.