Helping credit unions achieve growth, stability & member impact through smarter mergers

The number of credit unions continues to decline due to market pressures, regulatory burdens, and shifting member expectations.

Many mergers are negotiated behind closed doors, leaving little transparency or competitive process.

Our consulting service leverages our proprietary Merger Network that revolutionizes how credit unions approach mergers by leveraging data and a nalytics to match the right partners based on mission, financial alignment, and member needs.

Limited personal network

Non-Competitive Process

Non-Standard Process

Lack of Objective / Biased Advice

Lack of Transparency

Consider hundreds of candidates

Competitive Process

Standard Process

Objective / Unbiased Advice

Full Transparency

Unlike traditional processes, our network is transparent, competitive, and data-driven.

The old merger model relies on closed-door deals. We built a network that flips the script.

01

Decision Making

We conduct in-depth financial, regulatory, and operational analysis to ensure potential partners align with your credit union’s goals—saving you time, reducing risk, and streamlining the decision-making process.

02

Account Level Data

We analyze account-level data, business models, and technology stacks to match the best merger partners for you.

03

Partner Pool

Get access to hundreds of potential partners, rather than a limited network through personal connections.

04

Impact Assessment

We assess how a merger would impact real members–including interest rates, lending policies, and financial benefits.

05

Explore Opportunities

You can explore merger opportunities without committing resources upfront or revealing your interest publicly.

06

Data-Backed Recommendations

Unlike traditional approaches, we provide data-backed recommendations, not opinions.

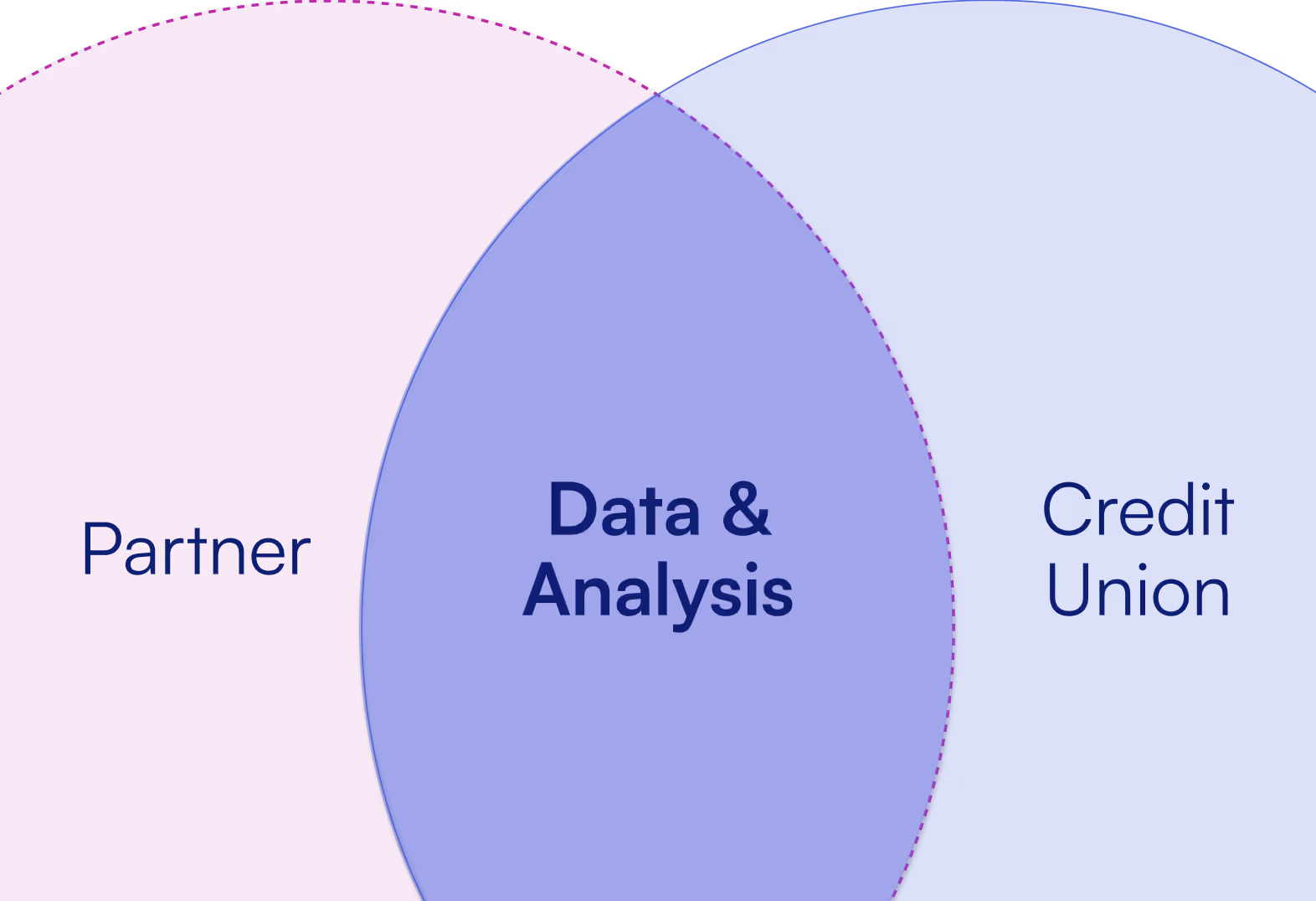

Not all mergers are created equal—finding the right strategic partner requires more than just asset size and geography. Our Merger Network goes deeper, leveraging proprietary data to assess how well a continuing credit union would serve the merging credit union’s members across key financial and operational factors.

Partner

Data & Analysis

Credit Union

Fit matters. We go beyond surface-level metrics to find partners who align with your goals, network, and members’ needs.

We analyze business models, field of membership, technology stacks, and financial structures to identify the most compatible merger partners

We assess which credit unions have the infrastructure and service network that would best support a merging credit union’s members

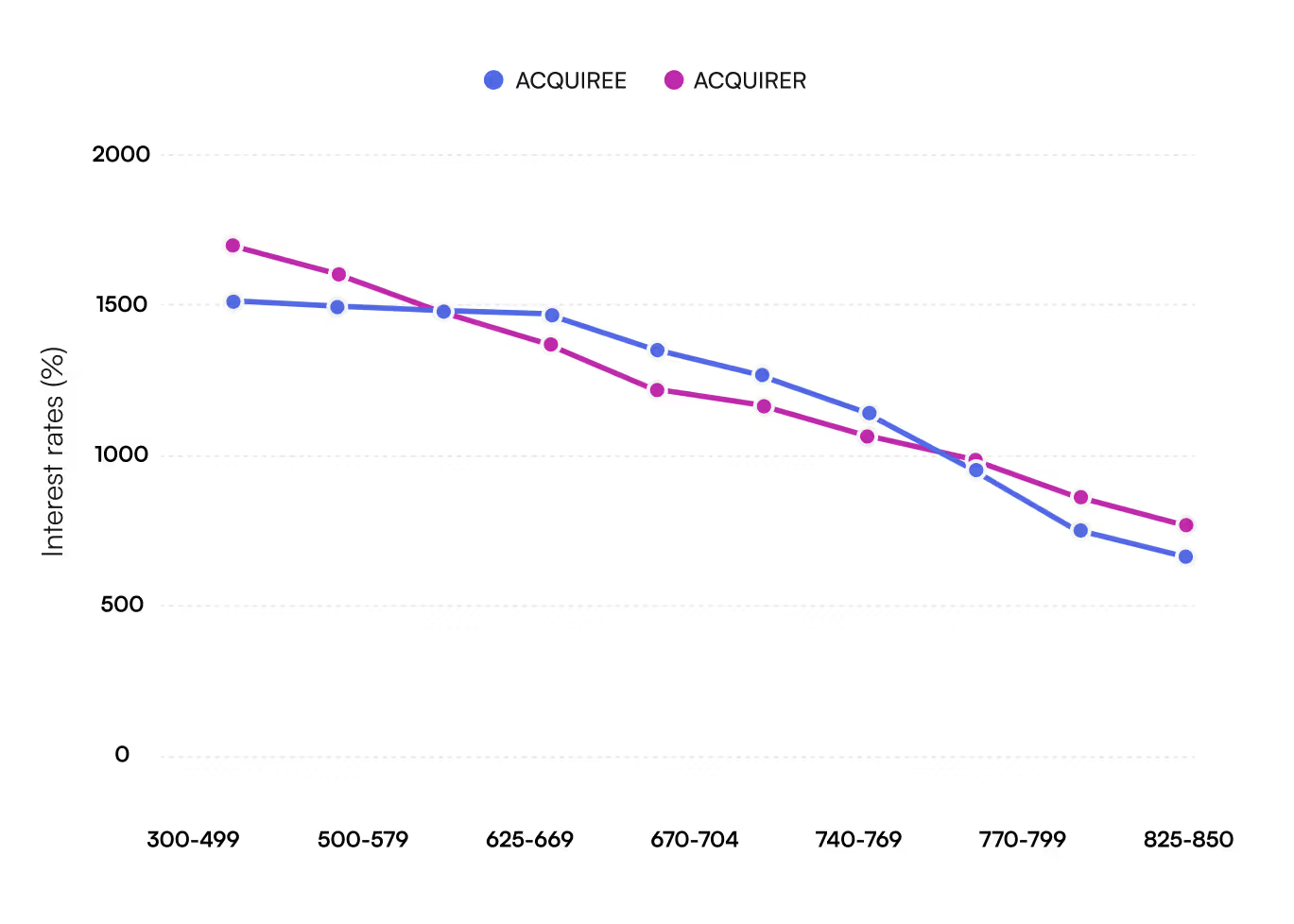

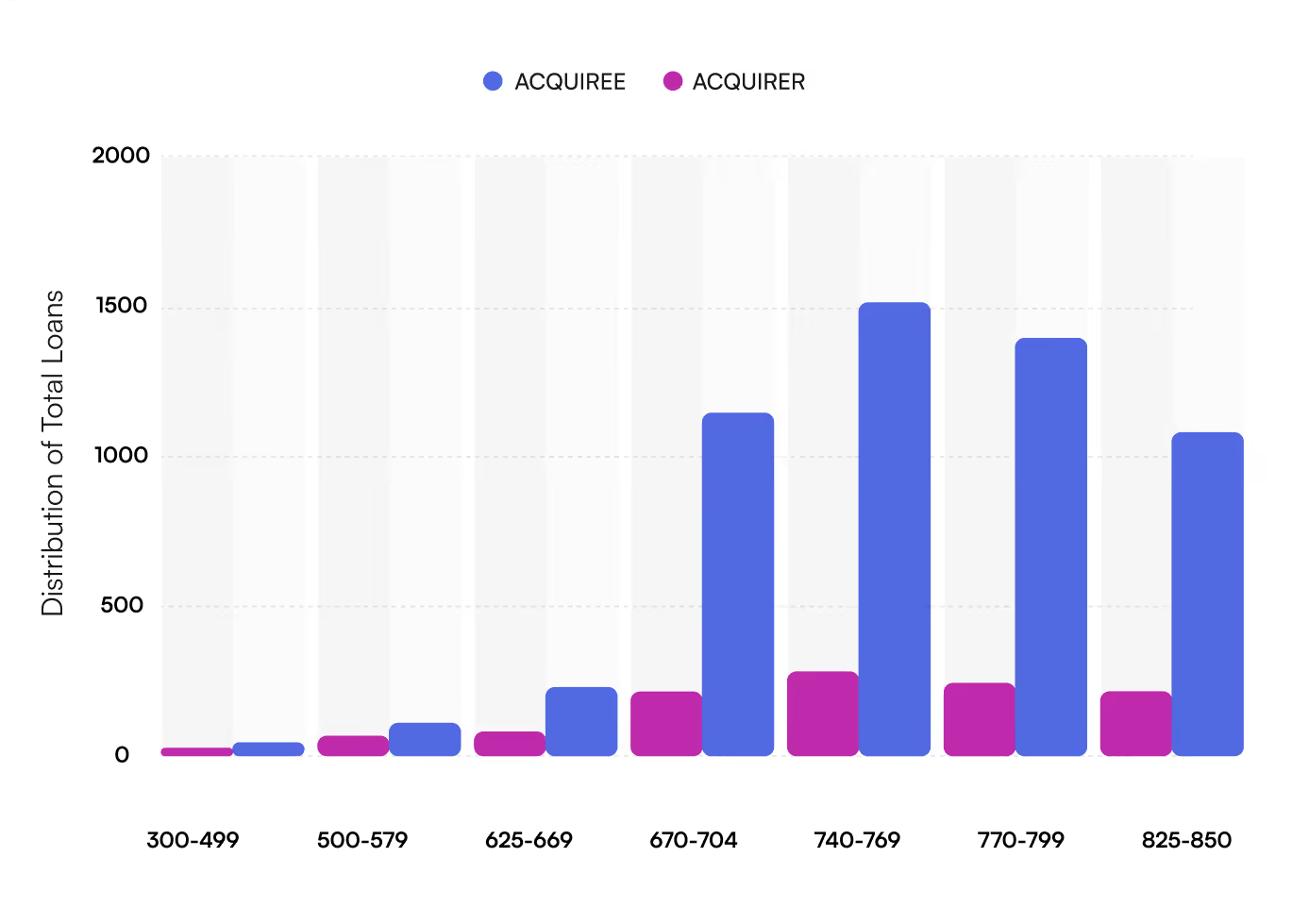

The member benefit analysis quantifies the dollar benefit to a merging credit union’s members by evaluating loan pricing, deposit rates, and financial product accessibility in a potential merger

Example

We analyze the interest rates charged by the merging credit union and the potential continuing credit union across credit scores.

Example

We examine loan distribution across credit scores at the merging credit union and the potential continuing credit union.

We streamline the merger process for both merging credit unions and continuing credit unions to create a more efficient, fair, and informed decision-making process.

Step 1

Data Upload & Mapping

Provide AIRES file uploads and code mapping

Step 2

Ideal Candidate Analysis

Complete a survey to determine your requirements and cultural fit

Step 3

Matchmaking

Model

We perform a detailed analysis on your data to rank potential merger partners and reach out to ideal candidates.

Step 4

Determine Finalists

Select 3-5 potential partners for facilitated introductions

Step 1

Data Upload & Mapping

Provide AIRES file uploads and code mapping

Step 2

Ideal Candidate Analysis

Complete a survey to determine your requirements and cultural fit

Step 3

Initial Outreach

We reach out to potential partners based on your ideal candidate analysis

Step 4

Merger Pitches

Participate in introductory calls and detailed analysis presentations to assess potential partners

While many credit unions pursue mergers as a means of expansion, some find mergers of equals (MOEs) to be a powerful strategy for long-term sustainability. Unlike traditional mergers, where one credit union absorbs another, an MOE is a true partnership—allowing both institutions to maintain influence, retain cultural identity, and combine strengths to better serve their members.

MOEs are gaining momentum among mid-sized credit unions as a way to achieve:

Stronger Financial Positioning – Shared investments in technology, marketing, and operational efficiencies

Balanced Governance & Leadership – A structured approach to integrating leadership while preserving institutional values

Enhanced Member Benefits – Expanded services, improved pricing, and greater community impact

Our team brings decades of experience in credit union mergers, strategic planning, and financial modeling.

Chris has more than 11 years of experience in consulting with a focus on data analytics, managerial cost accounting, workload modeling, performance and financial management. Before joining CUCollaborate, Chris helped clients develop and mature analytical capabilities to inform strategic business decisions at Grant Thornton, Deloitte and Callahan & Associates.

Luis has over 20 years’ experience researching credit unions, their historical and current call reports, and AIRES files, across a wide variety of topics including: financial sustainability, member-centric performance, asset growth drivers, capital requirements, and credit union openings, mergers, and closures. Before joining CUCollaborate, his clients included, among others, the Filene Research Institute, the National Credit Union Administration (NCUA), the Credit Union National Association (CUNA), Opportunity Finance Network (OFN), and other research institutions, government agencies, consulting firms, and university professors. At CUCollaborate, Luis’s current focus is developing methodologies that help credit unions use their AIRES files (1) to better measure their member benefits across demographic groups and to better serve the credit needs of their whole communities, (2) to better measure and manage branch performance, (3) to select new branch locations, and (4) to help acquirees in mergers select the acquirers that best fit their members’ needs. Luis received his B.A. in economics and mathematics from the University of Southern Mississippi and his PhD in economics with specializations in statistical analysis and finance from Auburn University, Alabama. His research has been published by the Filene Research Institute, the Federal Reserve Bank of San Francisco, Opportunity Finance Network, the Journal of International Financial Markets, Institutions and Money, the International Review of Finance, the Corporate Finance Review, Essays in Economic and Business History, and the Cooperative Business Journal.

Sean is a results-driven Senior Account Executive with over 10 years of experience in account management, including the past 8 years specializing in business development and client relationships within the consulting space. His professional journey spans diverse industries such as consumer goods, insurance, finance, banking, energy, sports and entertainment, automotive and aviation, and technology. Most recently, Sean worked closely with C-level leaders in assurance functions such as legal, compliance, privacy, and audit/risk. In his current role at CUCollaborate, he aligns tailored solutions with client challenges, manages pre-membership relationships, and leads strategy for key clients and prospects, all while delivering a first-class client experience and driving meaningful growth. Outside of work, Sean enjoys basketball, golf, biking, and spending time near the water with his wife Alison, their two-year-old daughter Grace, and close friends. A passionate sports fan, he cheers for the Tennessee Volunteers and DC’s professional teams and is guided by the mantra, “One day at a time, DOMINATE your day.”

Uncover how the Merger Network can pinpoint your best-fit merger partner.