Achieve Your Largest Expansion Opportunity

Field of Membership is your gateway to sustainable, strategic growth. Whether you're looking to convert your charter, expand into underserved areas, add associations or more, we help you achieve your goals with smarter, faster paths to expansion.

We help you identify and execute field of membership (FOM) and chartering changes that support your growth objectives. With deep expertise navigating complex state and federal regulations, we work with both federal and state-chartered credit unions across a range of initiatives.

Federal credit unions that are looking to reach more potential members need a partner with fluency in the NCUA Field of Membership Manual. We develop a deep understanding of your credit union’s differentiators and vision for the future to identify compliant FOM options that best align with the strengths and goals of your credit union.

Track record: We've successfully guided credit unions across the country to obtain approval for strategic Federal FOM changes.

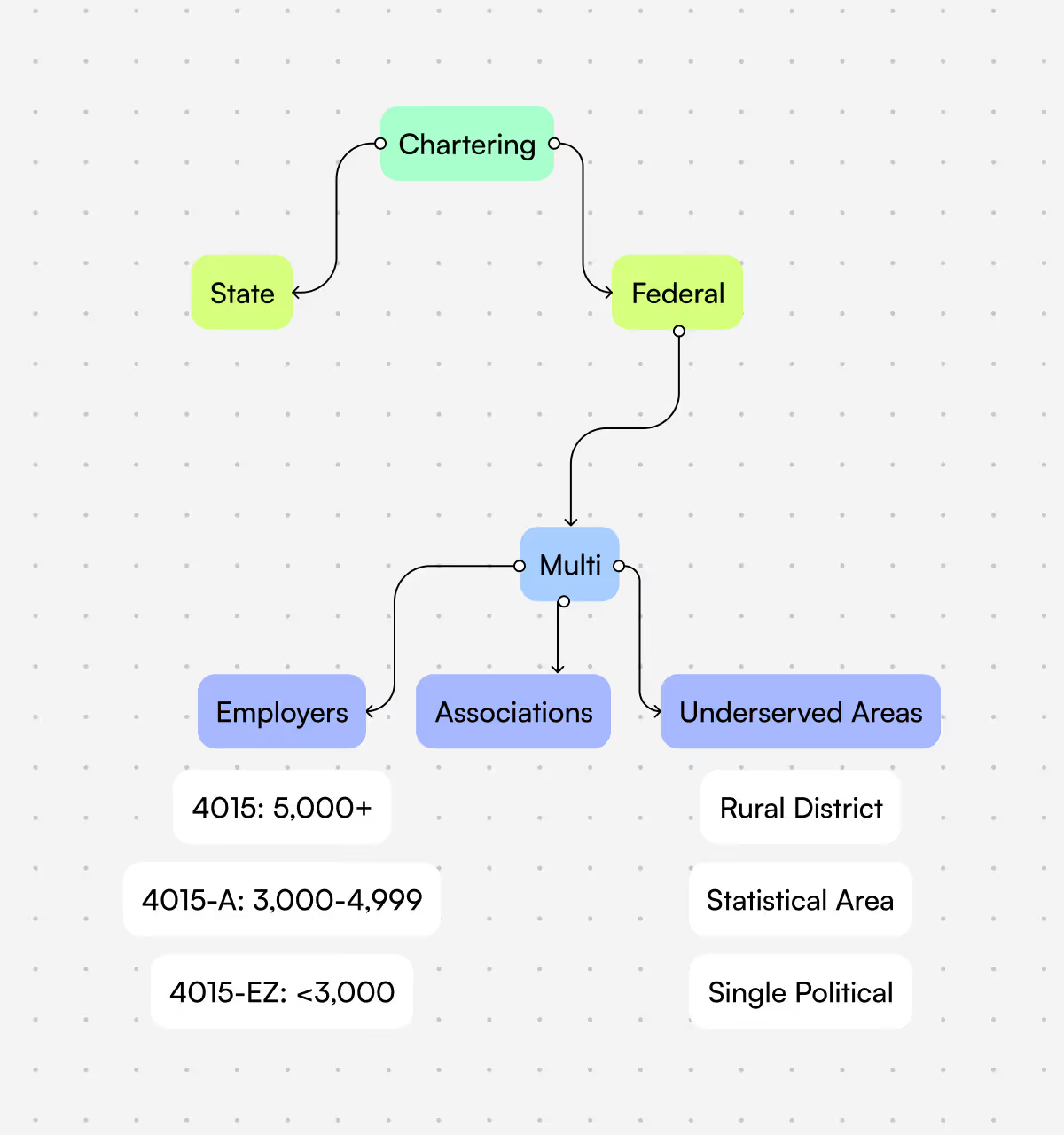

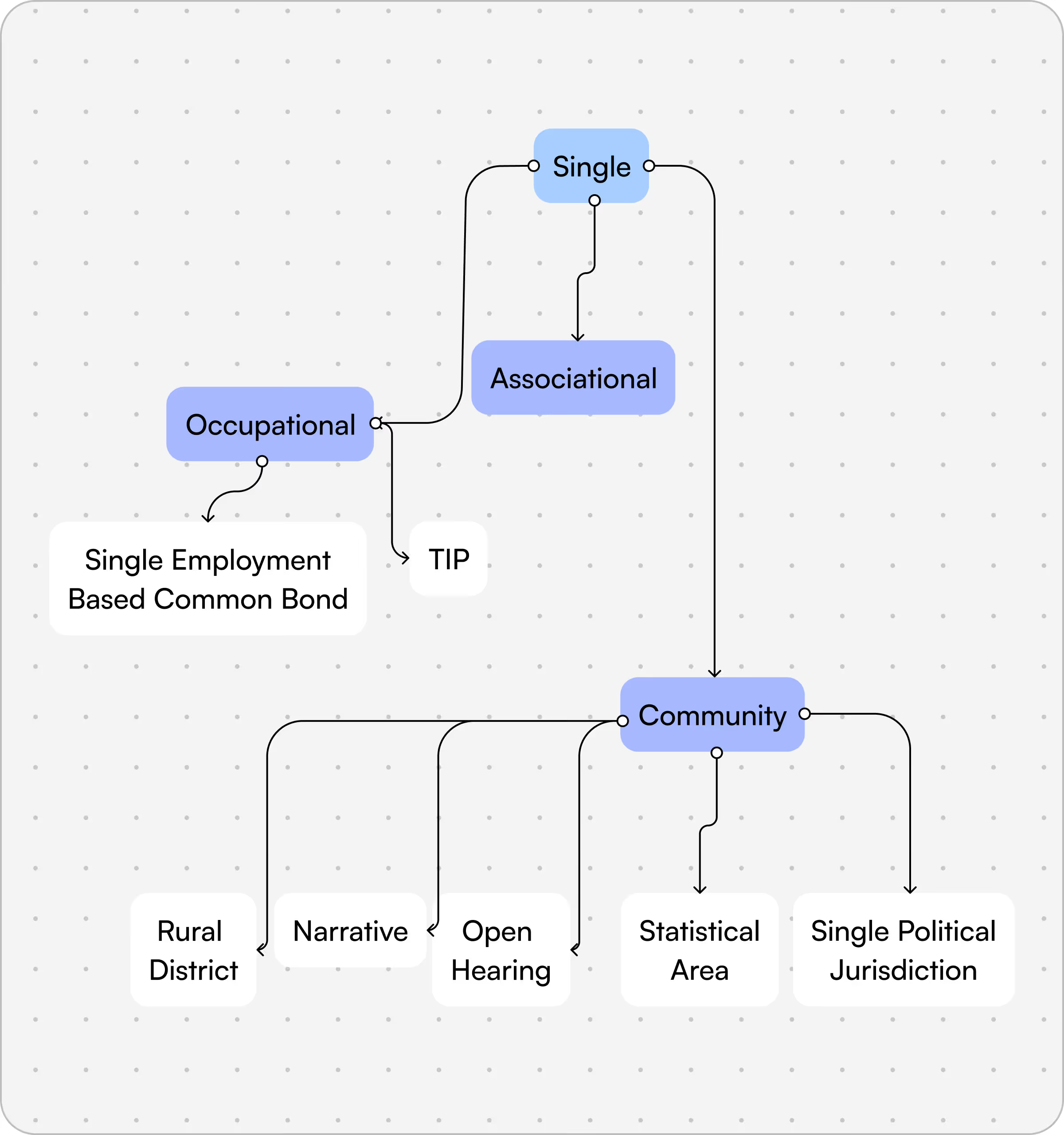

The Field of Membership options for Single Common Bond Charters include occupational, associational, or Trade Industry & Profession (TIP). Credit Unions exploring this charter type should consider the depth and strength of their relationship with a single sponsor, their penetration of the sponsoring organization, and the size of the credit union’s potential membership pool against strategic goals.

Credit unions with a single SEG partner and highly tailored products and services might find that a Trade, Industry & Profession charter allows them to expand their field of membership while continuing to serve a niche market need.

We help Single Common Bond credit unions, and credit unions considering the Single Common Bond charter type understand potential differentiators, assess opportunities, identify compliant FOM language, consider implementation of any changes, and navigate regulatory approval.

Track record: We've helped small and midsize credit unions transition into new charters that better reflect their member bases and open growth opportunities.

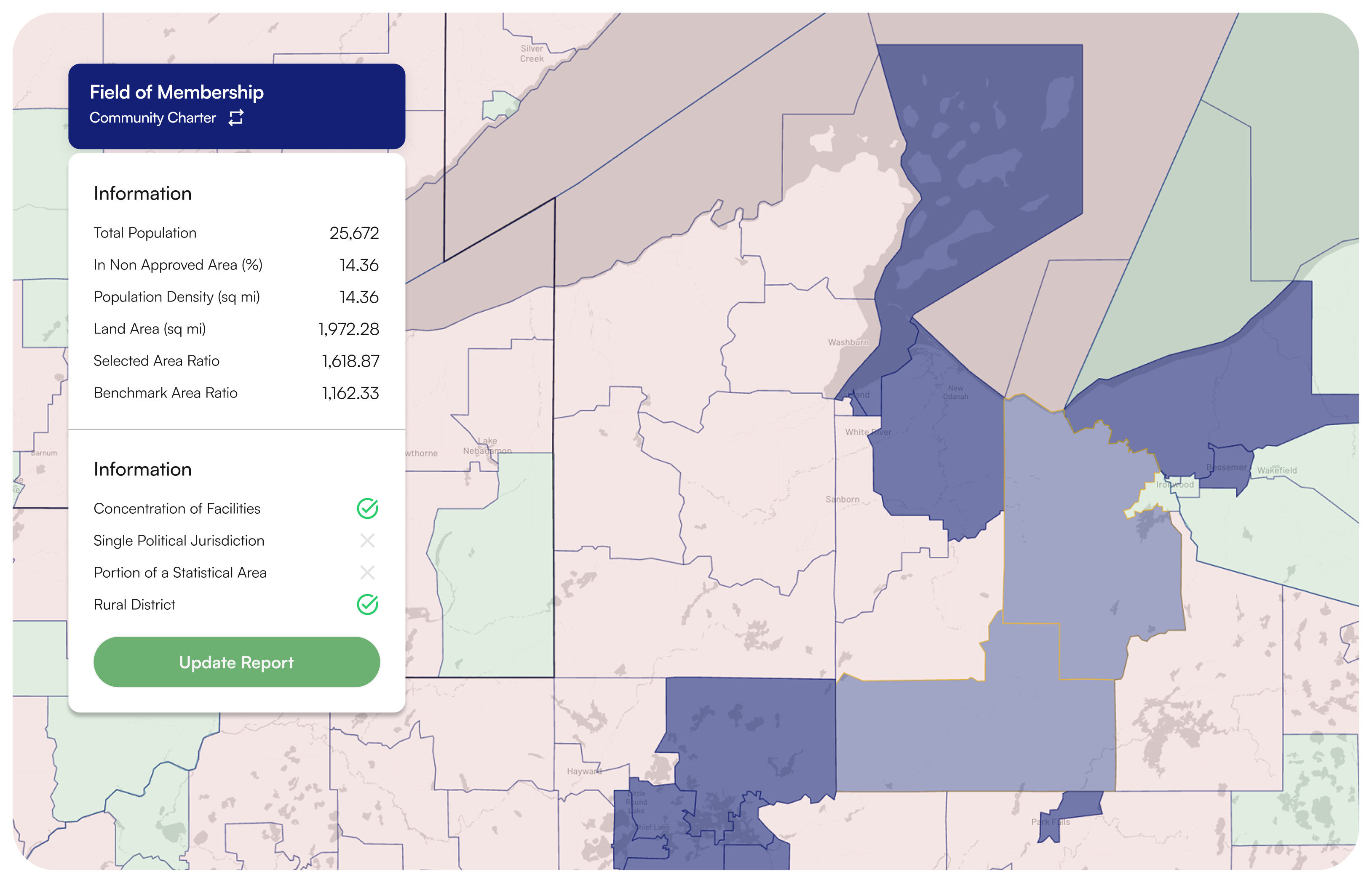

We help you identify eligible options such as a township, county, or municipality, and we guide you through the key trade-offs and opportunities that come with choosing a defined jurisdiction.

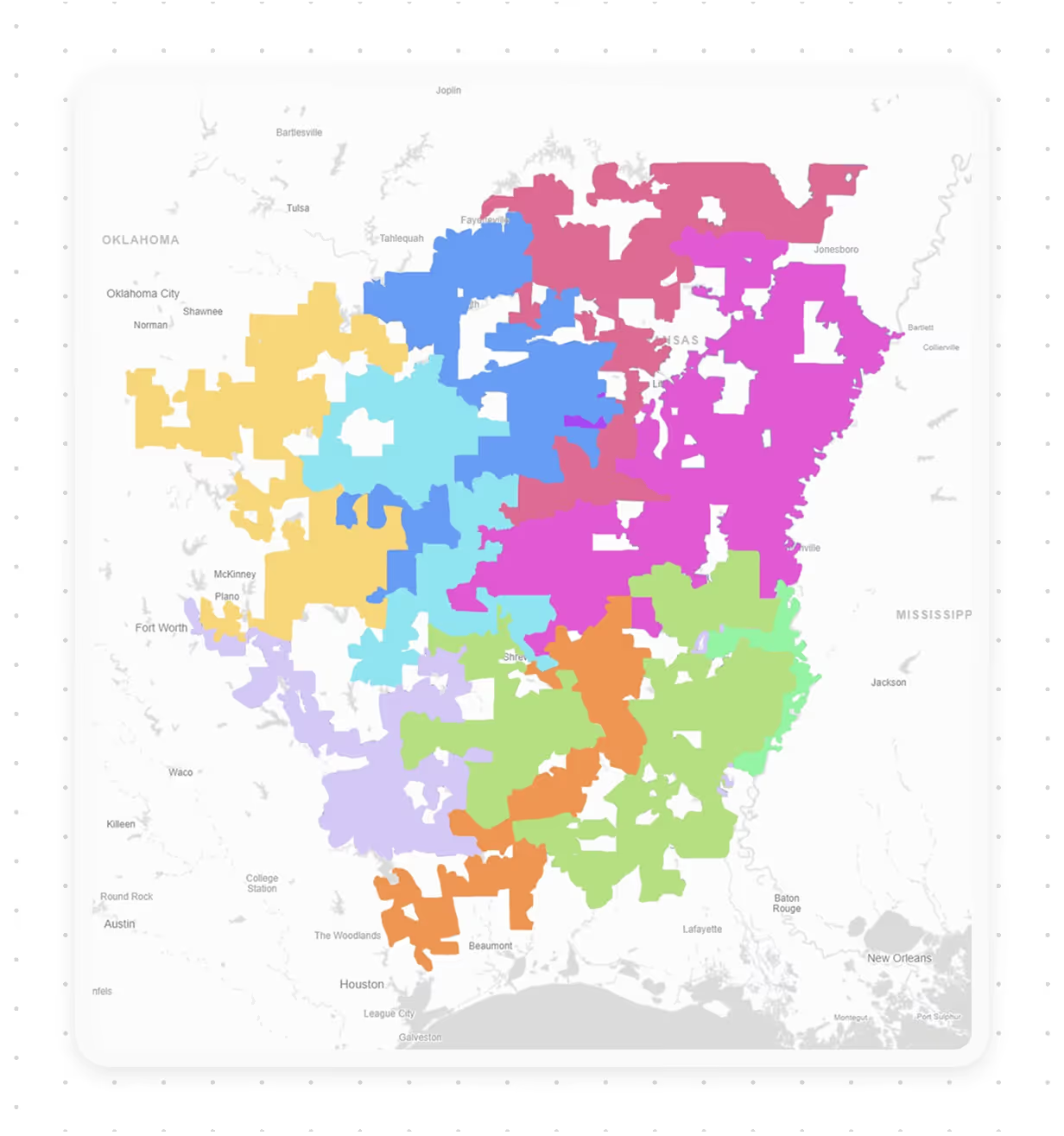

For metropolitan communities with populations under 2.5 million, our software efficiently computes and visualizes compliant statistical areas. This allows for effective scenario comparison, boundary analysis, and selection of the most suitable option for your market objectives.

Rural districts can be a powerful path for credit unions outside major metros, with specific population and density requirements. We model multiple scenarios to uncover non-obvious compliant pathways and maximize alignment between your FOM and long-term growth plans that often reveal options credit unions wouldn’t find independently.

When a community must be supported through a narrative, we bring deep expertise in meeting the NCUA’s rigorous research standards. We start by assessing approvability early to avoid wasted effort, then execute the research and drafting efficiently using proven frameworks and supporting evidence.

If a narrative community exceeds 2.5 million in population, an open hearing is the final step. CUCollaborate has successfully supported approval for the only open-hearing narrative community in history—helping with strategy, preparation, and execution.

CUCollaborate helps credit unions get the most from a Multiple Common Bond (MCB) charter, which offers three pathways to expand eligibility: Select Employer Groups(SEGs), Qualifying Associations, and Underserved Areas. For credit unions that are running into the limits of community charter definitions, we bring the strategy, analytics, and application expertise needed to build a successful Field of Membership (FOM) expansion without guesswork.

We start with a structured assessment of your current (or planned) MCB Field of Membership to identify the strongest opportunities across the three pathways and determine what will be most compelling and most efficient for regulatory approval.

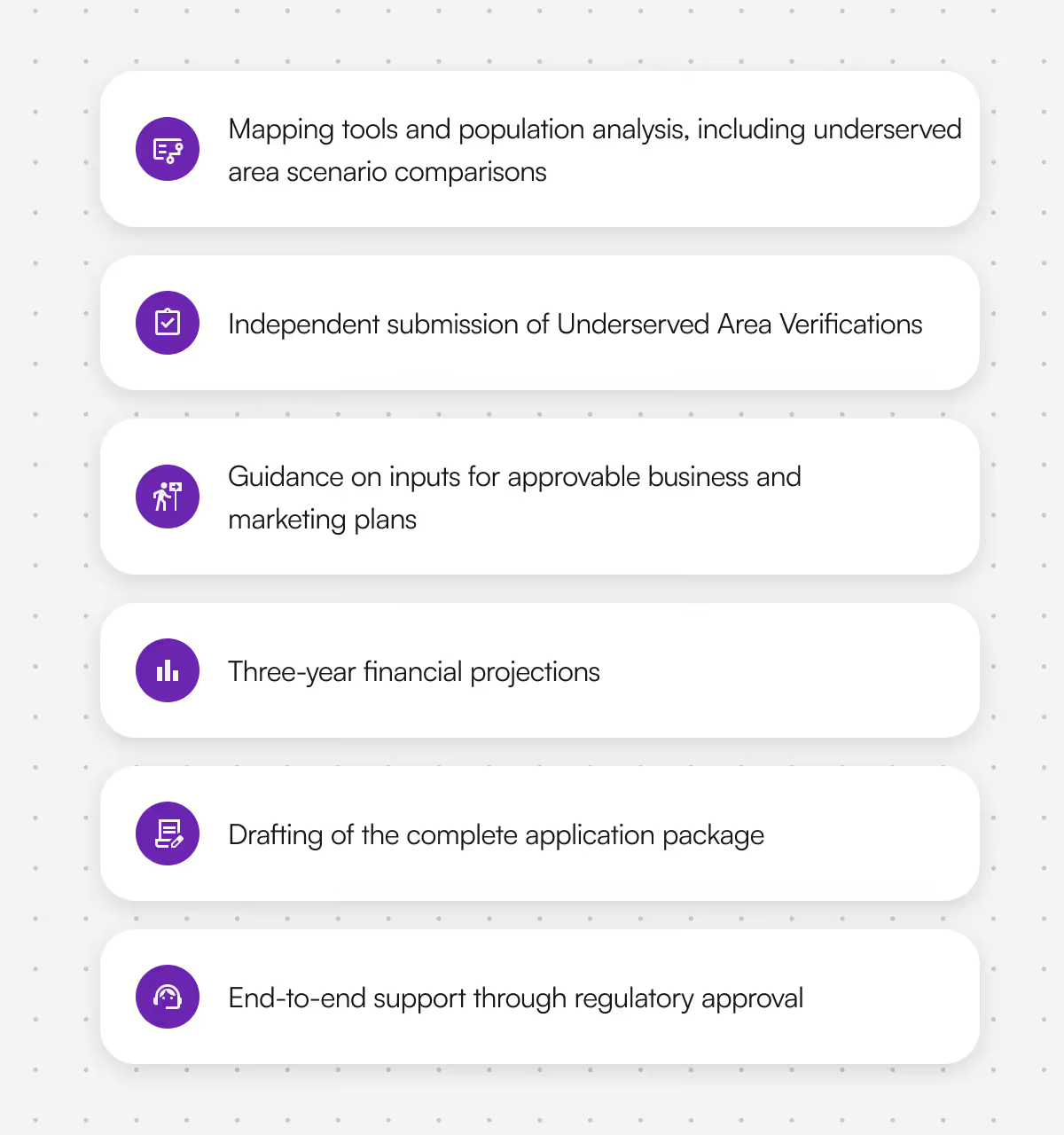

Our software includes algorithms purpose-built to draw regulatory compliant underserved areas that capture as much of your priority geography as possible. We help you interpret and apply the NCUA’s underserved-area criteria, run scenario comparisons, and evaluate where the best opportunities exist. Underserved areas can also support broader objectives such as expanding access to traditionally underbanked populations, improving ROI on community partnerships and branding, simplifying eligibility, and strengthening local ties. As underserved areas become larger or more complex, the business and marketing plan expectations increase. We guide you through what the NCUA will expect, gather the right inputs from your team, and translate them into a clear, approvable plan.

We help credit unions evaluate whether an association meets NCUA common bond requirements and whether it is realistically approvable. We also support credit unions in identifying and partnering with open associations that have broad eligibility criteria, enabling service to individuals regardless of where they live or work. When the process is complex, our team manages the details and guides you through to completion.

Adding SEGs is another way to expand membership. Because NCUA requirements scale with SEG size and structure, we help you navigate the nuances, assemble supporting information, and position your SEG additions for approval.

State credit union field of membership regulation varies across the country. We tailor our support to state-specific requirements. Our team bridges regulatory interpretation between state and federal guidance where needed.

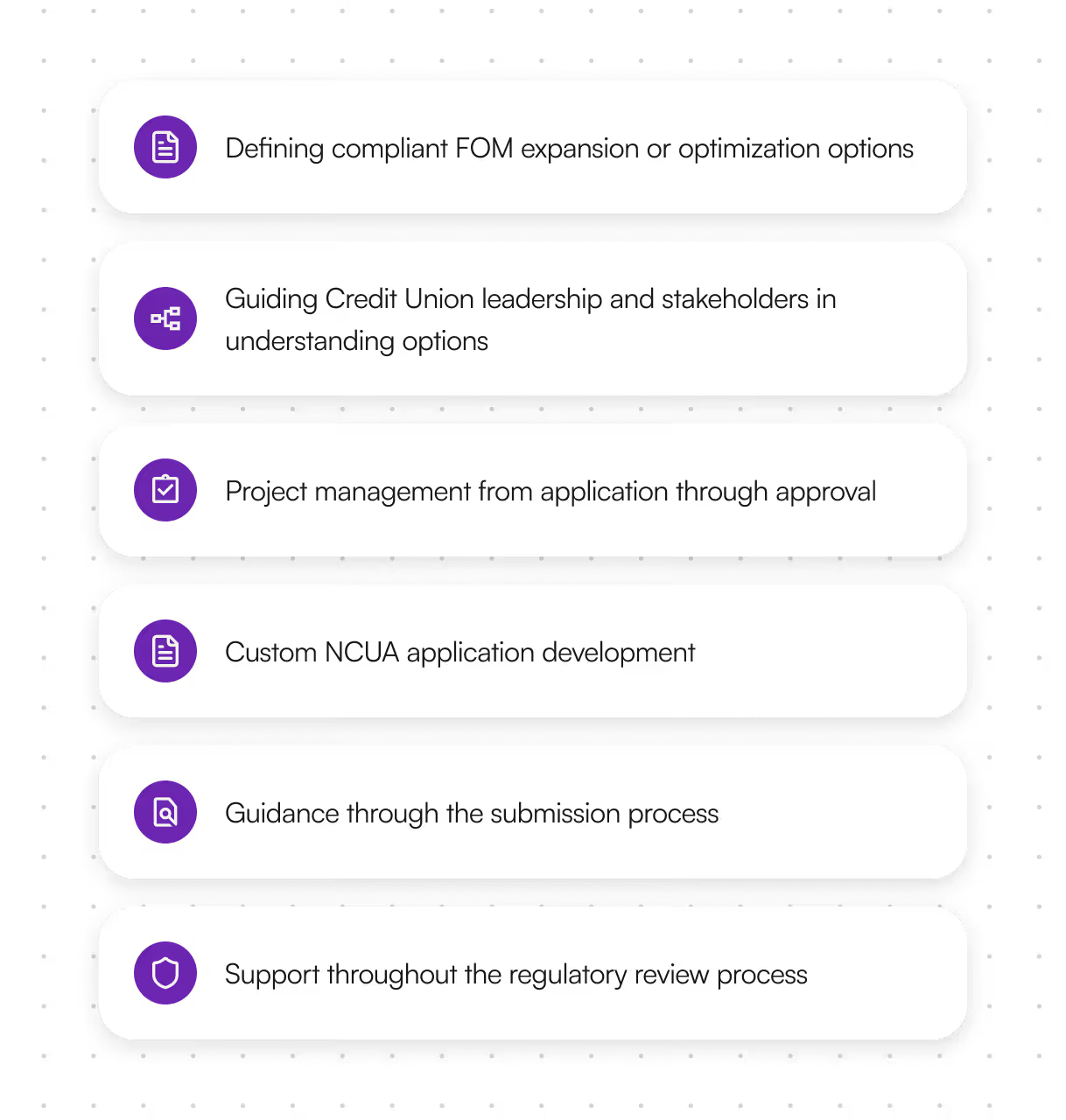

What we offer:

Project management from scoping to submission

Coordination with state regulators

Application deliverables aligned to unique state requirements

Support on member communications, notices, and voting

Track record: CUCollaborate has helped credit unions in 26 different states expand their field of membership.

Federal and State Charter Conversions are a fit for credit unions looking to maximize advantages with a comparison of the regulatory benefits offered by each. Field of Membership constraints, interest rate and lending limits, and borrowing and investment restrictions among other elements should be considered in the decision to convert.

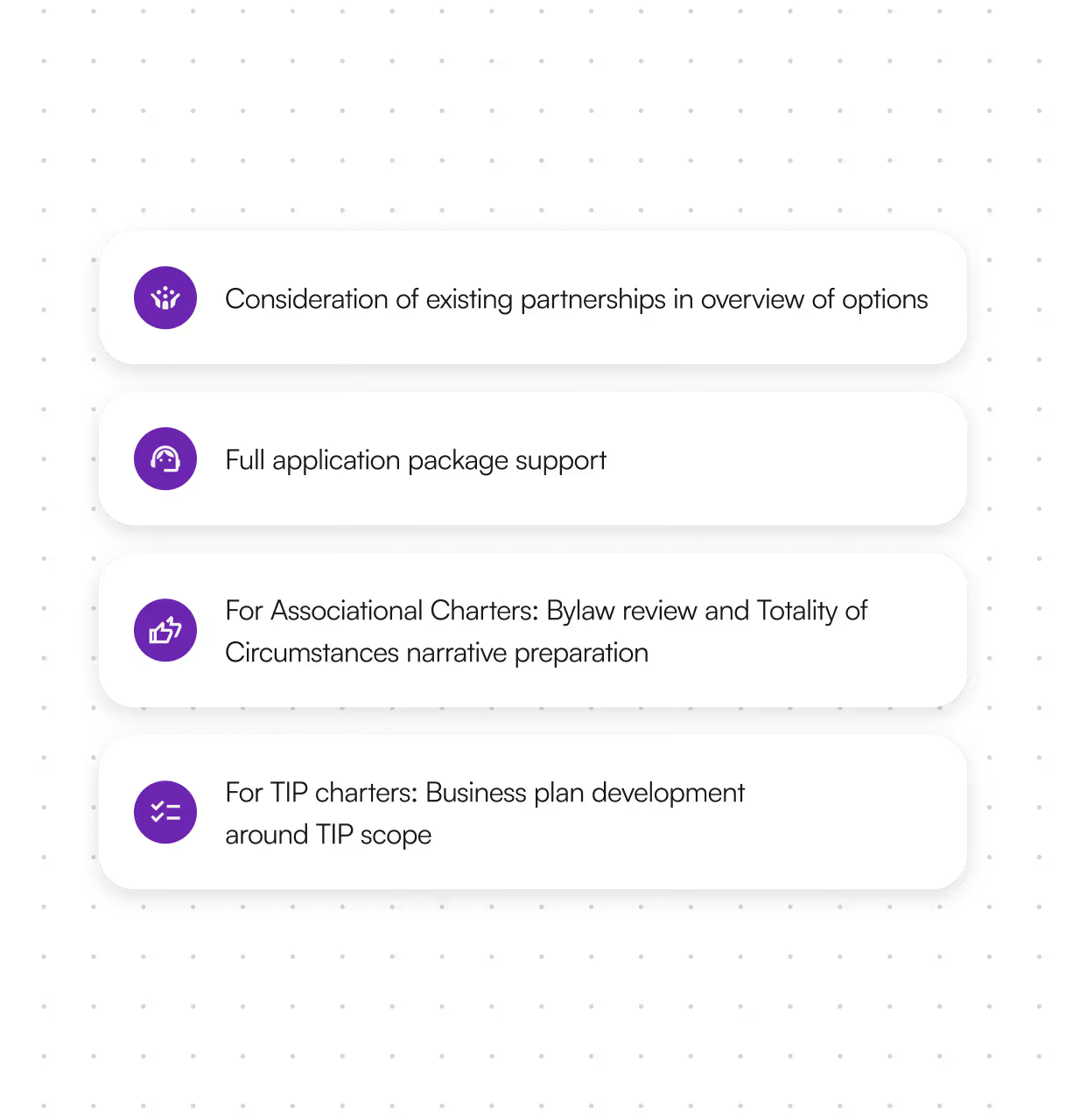

What we offer:

Side-by-side comparison of charter benefits and trade-offs

Coordination with both state and federal regulators

Identification of compliant and strategic FOM

Project management including guidance on collection of inputs

Drafting of conversion requirements

Guidance on submission

Support throughout the review process

Guidance on member vote and materials

Our custom-built software with precise mapping tools, predictive models and algorithms powers highest potential market opportunity scoping and identifies strategic paths for expansion.

Market and demographic analysis

From timelines to submission

Business plans, mapping, marketing strategy

Regulator relationships and responses

Workflow integration, compliance, and branding

Our team brings decades of experience in credit union mergers, strategic planning, and financial modeling.

Dom Patacsil believes in the power of stories. Whether that's data analysis or a work of fiction, he contends that stories help us make sense of the world and act toward greater growth. He has experience in administrative and operational consulting, with a focus on performance assessment. At CUCollaborate, Dom aspires to help credit unions empower the communities they serve through data-informed decision-making and long-term strategy.

With a master’s degree from the O'Neill School of Public & Environmental Affairs, Emily has experience working in local governments, with non-profit and community partners, and large federal agencies. Prior to joining CUCollaborate, Emily built managerial cost accounting models and oversaw increasing adoption of data modeling to improve transparency and business processes in federal budgeting. Emily strives to make her clients feel heard and aims to foster collaborative adoption and application of data and technology that enable credit unions to better serve local communities and achieve their missions.

With 15 years in the credit union industry, Janette has worked with institutions ranging from $400 million to $6 billion in assets, gaining experience across various roles—starting as a call center representative to most recently Vice President of Business Development. This journey has allowed for a deep understanding of credit unions at every level and fueled her passion for building strong relationships to help them grow. Her expertise lies in business development, strategic partnerships, and innovative growth strategies tailored to the unique needs of credit unions. As a Certified Credit Union Financial Counselor, Janette is also deeply committed to financial education and empowering members to achieve financial well-being. Outside of work, she's a proud sports mom, a Disney fanatic and an avid traveler, always planning the next adventure with her family.

Schedule a consultation with us to learn about how we can help your Credit Union achieve its growth goals.