Secondary capital and nonmember deposits growing in popularity

The NCUA has signaled that liquidity will be of particular concern for them, as Chairman Rodney Hood and Board Member Todd Harper both addressed the issue at NAFCU’s Congressional Caucus last week. Not only are low-income credit unions exempt from the member business lending cap, but they also have broader authorities to access liquidity in the form of secondary capital and nonmember deposits.

Typically, a credit union’s net worth entirely comprises retained earnings. Low-income credit unions, however, also have access to uninsured secondary capital, which can provide a healthy shot in the arm. Make no mistake – secondary capital shouldn’t be used reflexively to prop up a poorly performing credit union absent a holistic plan. But, among the many reasons for credit union leaders to consider a low-income designation, access to secondary capital is certainly a major one.

Olden Lane is a broker dealer and registered investment adviser that regularly works with credit unions on issues of funding and capital. Olden Lane CEO Michael Macchiarola explained that he sees CUs apply to accept secondary capital for a handful of reasons. One would be growth: “We see plenty of credit unions that would like to grow into their loan demand, but are constrained because, if assets grow faster than capital expands through retained earnings, it compromises the net worth ratio in the short term.” The second reason credit unions typically pursue secondary capital is for what Macchiarola refers to as “triage.” “Your capital position is impaired, and you could use a boost to plug a hole to fix a temporary problem. Perhaps secondary capital could work for you.” Here, however, he warns that triage capital without a broader strategy is not appropriate. In fact, Olden Lane’s research reveals that “secondary capital realizes its highest and best use when employed by substantial credit unions with reasonable economies of scale, or middle-to small-market credit unions with demonstrated growth prospects and sufficient capabilities to perform necessary planning and risk management to succeed with secondary capital.”

Should you position your field of membership to optimize a low-income designation? Ask CUCollaborate today!

Increasingly, a third group of credit unions is looking to secondary capital as a means to improve the net worth dilution that would accompany a merger or acquisition.

Finally, the fourth reason Macchiarola itemized, and one that was fairly common during the Great Recession of 2007-08, is the desire to stack additional defensive capital to handle consumers’ flight to safety. If a credit union is deluged with deposits as consumers retrench, the net worth ratio declines. For certain credit unions, the LICU designation and secondary capital are worth a look as forecasters continue to increase the country’s likelihood of an impending recession.

Secondary Capital for Low-Income Credit Unions

NCUA Rule 701.34 requires a low-income, federal credit union seeking secondary capital to present a secondary capital plan to the agency. At a minimum, the plan must:

- State the maximum aggregate amount of uninsured secondary capital the LICU plans to accept;

- Identify the purpose for which the aggregate secondary capital will be used, and how it will be repaid;

- Explain how the LICU will provide for liquidity to repay secondary capital upon maturity of the accounts;

- Demonstrate that the planned uses of secondary capital conform to the LICU's strategic plan, business plan and budget; and

- Include supporting pro forma financial statements, including any off-balance sheet items, covering a minimum of the next two years.

If a LICU is not notified within 45 days of the agency’s receipt of a Secondary Capital Plan that the plan is approved or disapproved, according to the regulation, the LICU may proceed to accept secondary capital accounts pursuant to the plan. The secondary capital account must be established as an uninsured secondary capital account or other form of non-share account.

While these uninsured accounts are required to have a maturity of at least five years, Macchiarola explained that nearly all of the current repayment plans carry a 10-year maturity with repayment of 20% over each of the last five years of the agreement.

Check out CUCollaborate’s Free Low-Income Designation Handbook!

Few Credit Unions Take Advantage of Secondary Capital

Secondary capital is anything but simple. And, Olden Lane always cautions credit unions to understand secondary capital within the credit union’s broader overall strategy and to be thorough in its preparation and diligence throughout the process. Secondary capital is subordinated to all other claims against the credit union’s capital, including the members, so investors are typically paid pretty handsomely for the risk they’re taking on. Plus, banks are eligible for Community Reinvestment Act credit in connection with a secondary capital investment. The current prevailing rate, according to Macchiarola, is between 5.75% and 6.25%, which is a significant cost of funds for the borrowing LICU. However, if a credit union really believes in the demand it has for loans, secondary capital can be immediately beneficial to earnings.

A simplistic example can illustrate the point: If, for example, an institutional investor provides $1 million in secondary capital at 6% to a credit union with 10% net worth, then the credit union uses that $1 million to support roughly $10 million in loans, he explained. Say the credit union’s spread is 300 basis points between what it pays for money and where it writes loans. Essentially, it is paying 60 basis points on the secondary capital once it is cycled through the business and not 6%. In such a case its net return becomes 240 basis points. Of course, a whole host of additional qualitative and quantitative considerations will inform a credit union’s decision to pursue secondary capital.

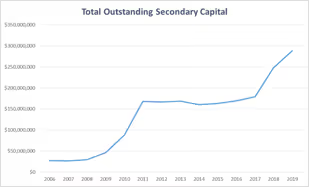

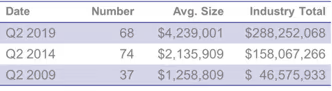

Still, very few credit unions are taking advantage of secondary capital. As of Q2 of 2019, only 68 credit unions have secondary capital on their balance sheets, accounting for $288M in total secondary capital balances, Macchiarola highlighted.

All LICUs are eligible for secondary capital and about half of credit unions are LICU-designated, Macchiarola said, adding, “There's tons of room for upside and there's tons of potential for people that do it responsibly.” But many credit union leaders feel it’s too long or complicated a road. Some don’t want to deal with the NCUA for nine months, can’t find time for the administrative burden or don’t like the payout, he added. Many simply don’t need it.

“The people who have actually failed with secondary capital tend to be smaller. They also tend to have

taken it when their net worth was lower…and they took it as a one-off and not part of a big, broader plan,” Macchiarola concluded. Over and over, he cautions that, to be successful, the process requires preparation and due diligence and a thoughtful, holistic approach to the credit union’s overall strategy.

Nonmember Deposits

On the funding side, nonmember deposits, in particular, could rise in importance for a number of reasons. First, with loans-to-shares ratios across the industry at 40-year highs, most lenders are seeking reliable and less costly funding options. Traditionally, credit unions and community banks offer higher rates on CDs to quickly bring in funds, but the big banks are making this game more difficult every day. “The big banks were really not what you worried about in the local deposit market,” Macchiarola observed. “But now increasingly the big banks are swooping in for those deposits because they need to gather those the deposits to help keep the ratio that the regulators are insisting that those banks keep.” Additionally, newer fintech and digital channel offerings are making it more efficient for depositors, further increasing competition. Perhaps the most noticeable manifestation of the increased competition is the sharp rise in the growth of share certificates, the most expensive organic funding source available to credit unions.

Over the past year, the cost of funds across the industry increased from 70 bp to 97 bp, a 40% increase. Macchiarola said, “That’s why credit unions have to think about funding sources and the cost of funding like never before.”

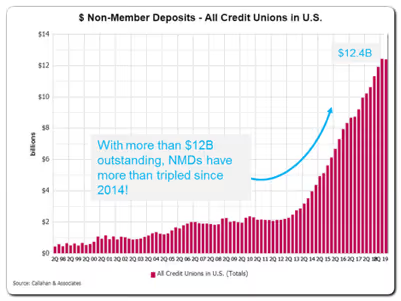

The NCUA is encouraging credit unions to not only pay attention to liquidity levels, but also the diversity of their liquidity sources. Following the 2007-08 economic crisis, a lot more credit unions became members of the Federal Home Loan Banks. The number of credit unions accepting nonmember deposits has also tripled. While the overall number is still small – about $12 billion in nonmember deposits across roughly 1,000 credit unions, according to Macchiarola, that’s up from just $3 billion in 2014.

Read our previous blog on how LICUs stack up financially with all credit unions!

While NCUA Rule 701.32 allows federal credit unions to accept nonmember deposits from public units and other credit unions, low-income designated credit unions can accept nonmember deposits from other nonmember sources. Currently, nonmember deposits are limited to 20% of a credit union’s shares or $3 million, whichever is greater.

By such limitation, the current capacity for credit unions to accept nonmember deposits is about $250 billion. Yet, balances are only currently at $12 billion. “It’s just not the way credit unions have thought about it,” Macchiarola said. “There’s this bias to give the member the better rate by paying more for member deposits before accessing the nonmember market.” If the credit union wants to preserve its net interest margin, however, Macchiarola cautions that such a philosophy ”will lead to increases on the other side of the balance sheet, as the rate on member loans has to increase to account for the increased cost of funds.”

In addition, the NCUA Board is considering a proposal to increase acceptance of nonmember deposits up to 50% of shares to be consistent with the Federal Credit Union Act’s limit on borrowings.

So, if credit unions are not yet taking full advantage of nonmember deposits, why bother increasing the maximum? “Liquidity is front and center for the NCUA,” Macchiarola said. “Let’s acknowledge something refreshing about this regulator: They are forward thinking. They are actually looking down the road and they understand that credit unions are taking their liquidity from too few sources and they are too reliant on their members.” Plus, he added, today’s member deposits are harder to access, more costly and less reliable. “Liquidity is not a problem, until it is. And once it is, you can’t do anything to fix it.”