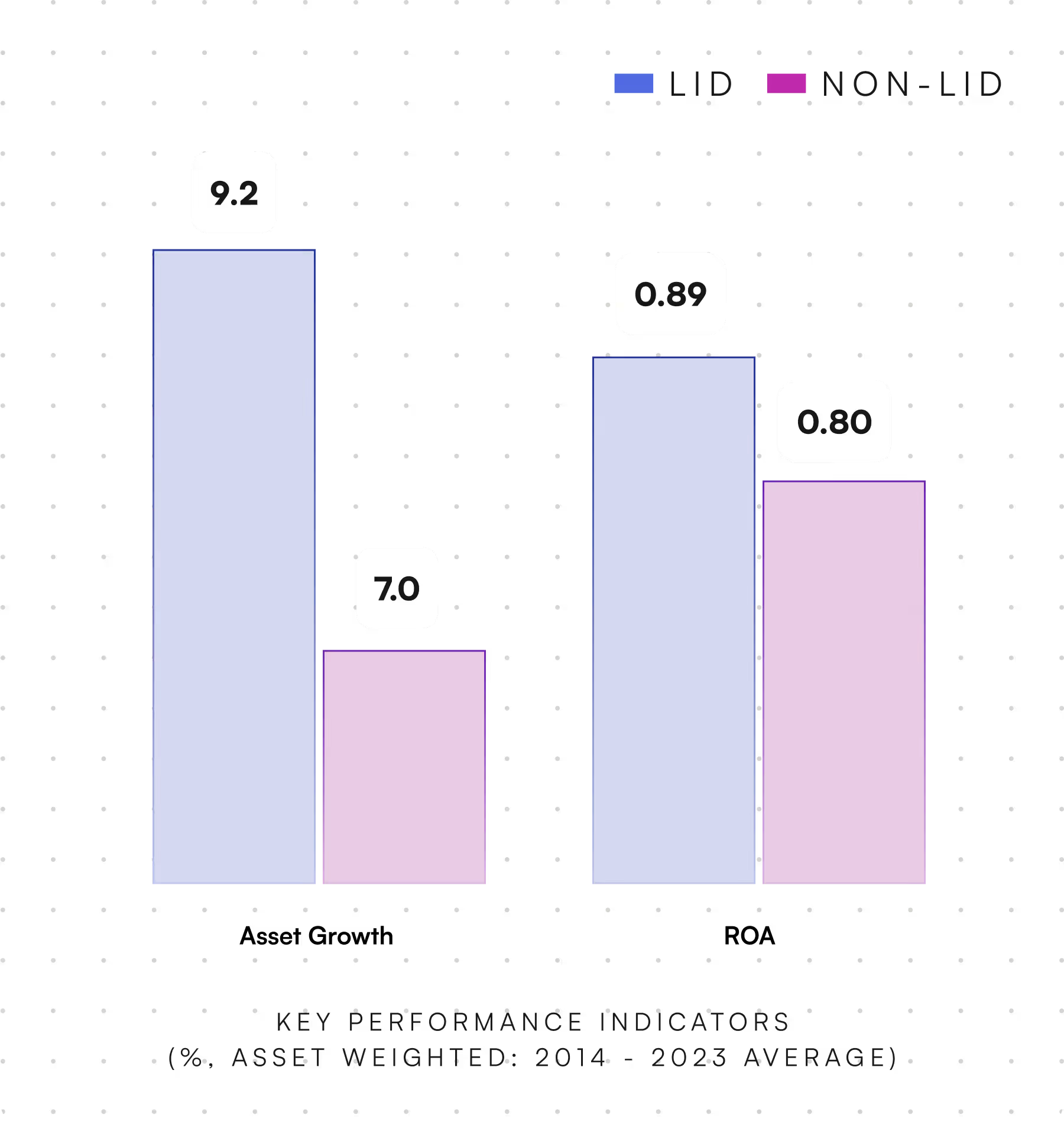

Data-Driven LID Support for Credit Unions

Business Lending Cap: Credit unions are restricted to a 12.25% cap on member business loans, limiting their ability to support local entrepreneurs.

Fixed Asset & PCA Rules: Regulations like the fixed asset cap and net worth requirements constrain growth and operations.

Missed Grants & FOM Growth: Without LID, credit unions lose access to financial grants and face challenges expanding into underserved areas.

But there’s a strategic solution that can give your credit union a real advantage:

A Low-Income Designation (LID)

Credit Unions with LID gain access to a host of benefits:

With our proven approach, any credit union can attain LID. We guide you through the path that makes the most strategic and practical sense for your institution.

The standard and most common route. Match member data to LID geographies.

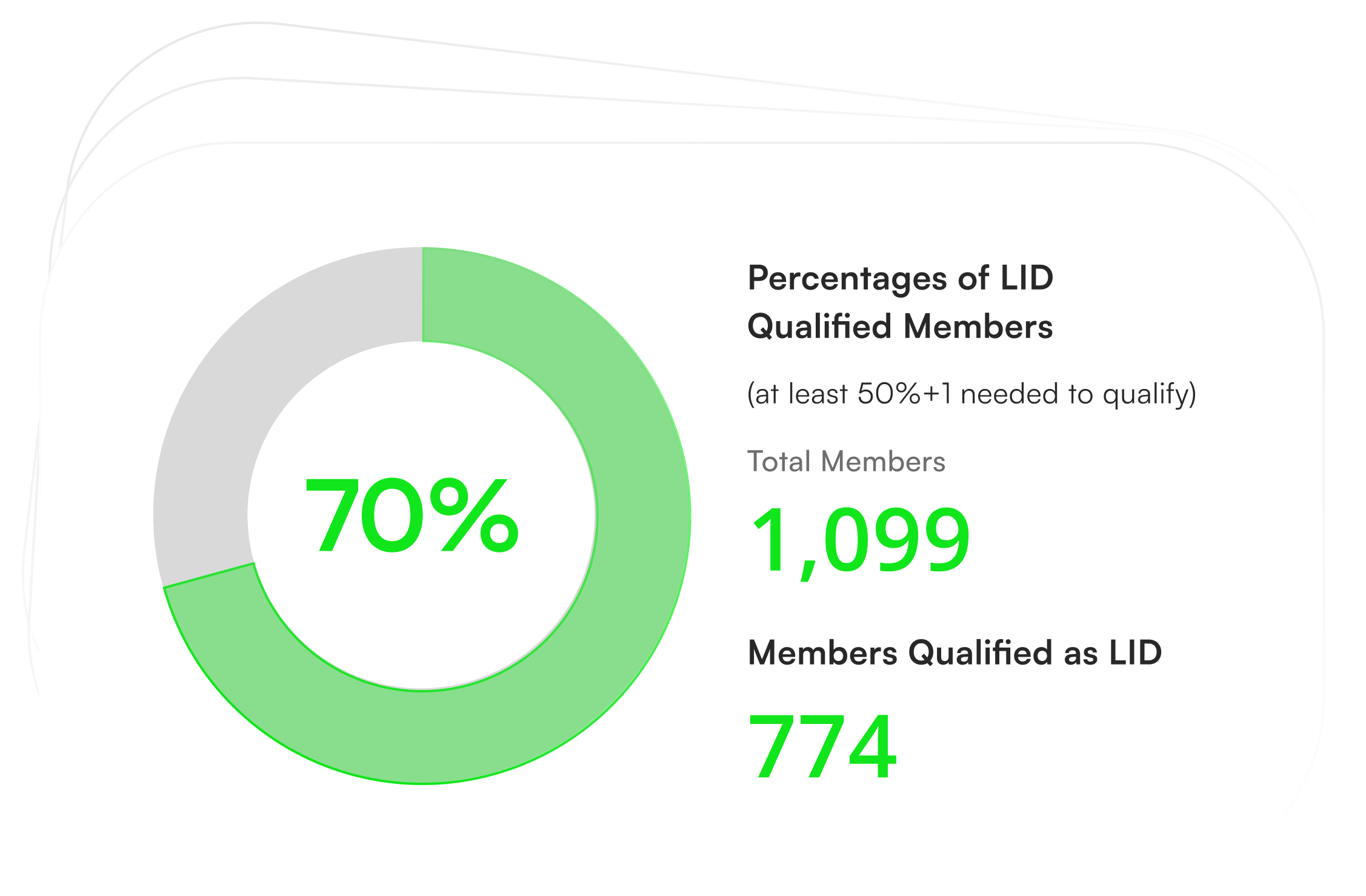

An option for federal community charters. Show that a majority of your total potential membership meets the low-income definition.

The right fit for a select few. Demonstrate the share of your loans issued to a low-income target population.

We provide credit unions with a path to attain LID with certainty. And once you attain LID, we make it easier for you to keep it.

Baseline Assessment: Review your current data and eligibility

Identify data enrichment needed to maximize your current membership potential with qualifying individuals

Easily build reports to demonstrate that a majority of the total potential membership meets the low-income definition.

Identify the % of Your Loans Issued to a Low-Income Target Population

Our fintech lending partners leverage CUCollaborate’s proprietary LID & FOM APIs along with the credit union’s membership application and loan documentation to provide our clients with a consistent pipeline of new members and qualifying loans

We make it easier for you to retain your status through tracking and monitoring tools, including LID dashboards, APIs, and custom mapping tools.

Regardless of where you are in your LID journey, we’ll help you use LID to fuel your mission, fund your growth, and serve your members better.